Most business owners launch their dream because they love their craft, not because they are passionate about spreadsheets. That familiar “shoebox of receipts”—whether physical or a messy digital folder—can quickly turn your midnight hours into a headache as tax season approaches. You likely already know that keeping your business income and personal income in separate bank accounts is a golden rule, but simply dividing your cash doesn’t tell you how well your company is actually performing. Industry data reveals that entrepreneurs often spend over a dozen hours every month just trying to untangle their own messy transaction records. Discover the best info about contador.

Navigating these numbers requires more than a basic calculator. Financial data should act as a GPS for your company’s future, guiding your daily operations rather than just appeasing the IRS once a year. Professional accounting actively protects your personal assets in three critical ways: by maintaining the strict legal boundary between your home and business finances, shielding you from costly compliance penalties, and uncovering legitimate deductions that lower your taxable income. Your numbers transform from a source of anxiety into a clear roadmap for proactive financial planning.

Recognizing who manages this GPS brings us to the crucial difference between a bookkeeper and an accountant. Think of a bookkeeper as “The Historian” who records the daily play-by-play, tracking exactly what money entered and left your business yesterday. An accountant steps in as “The Strategist” who analyzes that historical data to predict your future, advising you on when to hire a contractor or how to price your newest service. Both roles are highly valuable, but confusing basic data entry with high-level strategic analysis often holds growing businesses back.

Transitioning from early DIY tools to expert partnerships is a natural evolution for every successful venture. Early on, a simple spreadsheet or a basic mobile app might seem sufficient for managing the handful of expenses you have. However, as your operations expand across state lines or you start juggling complex client projects, finding the right accounting services for small businesses in the United States becomes essential for sustainable growth. Relying entirely on guesswork eventually costs significantly more than investing in proper guidance.

What if you could tell, at a single glance, exactly which of your products makes you the most profit per hour? Asking yourself, “Do I need an accountant for my small business?” is the first step toward moving from feeling overwhelmed by numbers to feeling completely empowered by them. Professional financial navigation protects your hard work and sets the stage for a thriving, profitable future.

Why Your Bookkeeper is the ‘Historian’ and Your Accountant is the ‘Architect’

Most business owners wear every hat, but letting an expensive CPA sort daily receipts is like hiring an architect to hammer nails. A bookkeeper acts as your financial historian, recording every dollar that moves through your business. They manage transaction categorization—putting every expense into the right bucket, like ‘software’ or ‘supplies’. Whether you choose outsourced bookkeeping vs in-house accounting, relying on a dedicated bookkeeper for this daily groundwork saves you thousands in high-level CPA fees.

Once that clean data is ready, your accountant steps in to build your financial future. While bookkeepers handle the daily play-by-play, professional accounting services focus on the big picture. Here is how their specific tasks differ:

- Bookkeeper: Logs daily cash flow, categorizes receipts, performs bank reconciliations, and runs basic payroll entry.

- Accountant: Makes adjusting entries (fine-tuning the books at year-end so your revenues properly match your expenses), designs tax strategy, and analyzes profit.

This clear pipeline from simple data entry to strategic application ensures you always know if your hard work is actually turning a profit. With daily tracking and year-end reporting cleanly separated, your financial foundation is finally strong enough for the next step: Navigating the IRS Maze: Essential Tax Compliance for Startups and LLCs.

Navigating the IRS Maze: Essential Tax Compliance for Startups and LLCs

The transition from employee to business owner brings a whole new set of rules, particularly regarding IRS tax compliance for startups. Your first major step is securing an Employer Identification Number (EIN) by filing Form SS-4. Think of an EIN as a Social Security Number for your company; it establishes a legal boundary, allowing you to open dedicated business bank accounts and protect your personal identity.

Because most small businesses operate as Limited Liability Companies, they enjoy “pass-through” status, meaning profits flow directly to your personal tax return. However, federal filing deadlines still shift based on your exact structure. A single-member LLC typically files by April 15th, whereas multi-member partnerships must submit documents by March 15th to satisfy strict financial reporting requirements for LLCs.

This flow of personal profit also triggers a notorious hurdle for new founders: the 15.3% Self-Employment Tax. In a traditional corporate job, your boss covered half of your Medicare and Social Security contributions, but independent owners face a “double hit” paying both halves. For instance, a local coffee shop owner must budget for this specific levy long before standard federal income taxes are even applied to their earnings.

To survive these rigid federal rules without overpaying, you need impeccably organized data throughout the year. Catching every single tax deduction requires knowing exactly where your money went, which leads directly to setting up the ‘Chart of Accounts’: Building the Filing Cabinet for Your Financial Success.

The ‘Chart of Accounts’: Building the Filing Cabinet for Your Financial Success

Most new business owners dump every receipt into a single spreadsheet, making it impossible to see where their money actually goes. Think of the Chart of Accounts as a digital filing cabinet where every dollar gets a specific folder. By categorizing costs, you finally reveal true profit margins. For example, separating general expenses from COGS (Cost of Goods Sold)—the direct materials and labor required to create your product—shows exactly what it costs to deliver that handmade candle or freelance project.

When setting up a business chart of accounts, you mirror the IRS Schedule C tax form, saving hours of frustration in April. A standard setup uses five common Chart of Account categories for small business:

- Assets: What you own

- Liabilities: What you owe

- Equity: Your ownership stake

- Revenue: Money coming in

- Expenses: Money going out

This structured approach prevents the dreaded “Miscellaneous” trap, a vague category where wasteful spending frequently hides out of sight.

Choosing between DIY software like QuickBooks vs professional accounting services comes down to how complex these folders become as you grow. A clean cabinet tells you if you are making money on paper. But paper profits cannot pay the rent, which leads directly to Cash Flow Management: Why ‘Profitable’ Businesses Still Go Under.

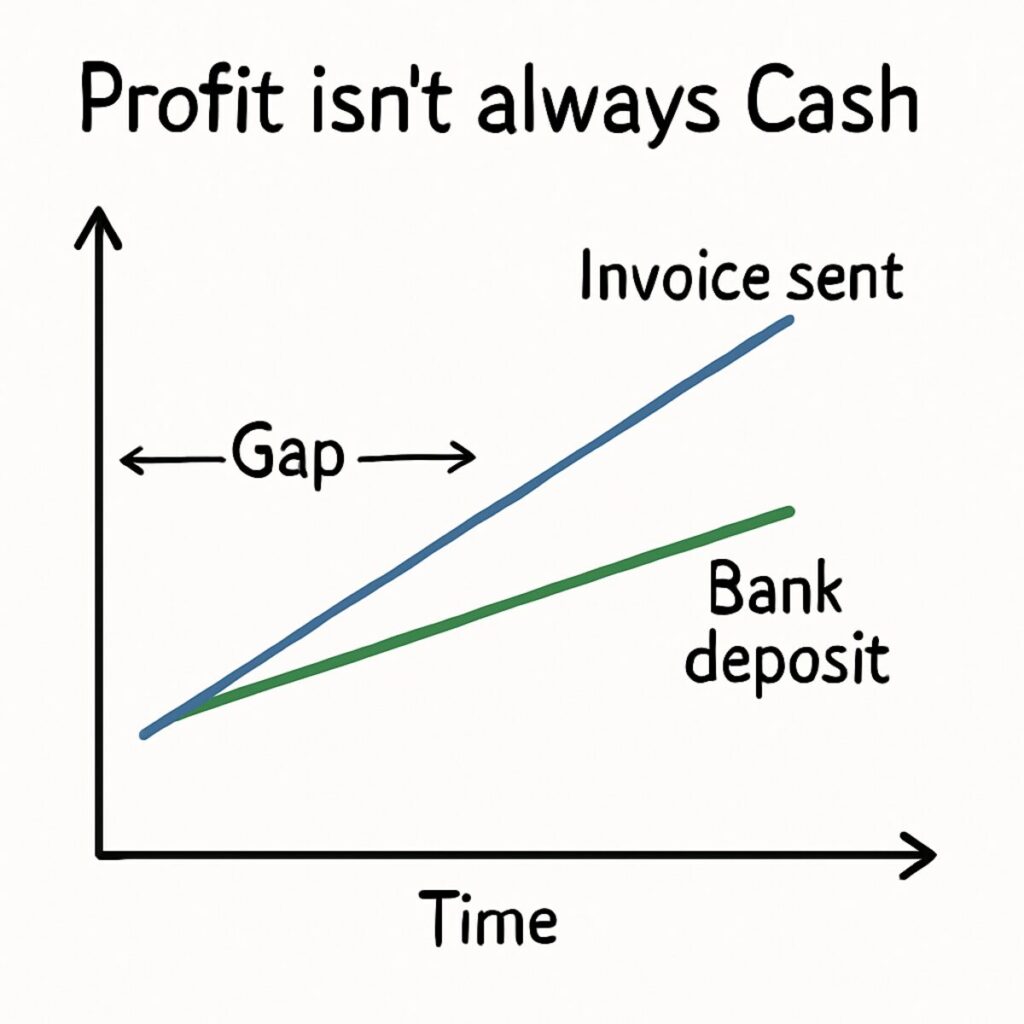

Cash Flow Management: Why ‘Profitable’ Businesses Still Go Under

Many business owners celebrate a record-breaking month of sales, only to panic when it is time to run payroll. This disconnect happens because generating revenue and actually collecting money are two entirely different milestones. Proper cash flow management for small companies prevents this nightmare by tracking the actual movement of dollars, ensuring you can survive the gap between delivering a service and getting paid for it.

Mastering this collection timeline requires knowing how your business records income. If you use the “Cash basis” method, you only count money when it physically hits your bank account. In contrast, the “Accrual basis” records income the moment you send the invoice, making you look highly profitable on paper even if your client has not paid yet. While accrual gives a great big-picture view of growth, relying on it blindly can ruin you when your rent is due today but checks arrive tomorrow.

To avoid this dangerous waiting game, smart founders rely on an accounts receivable aging report. Think of this tool as a financial radar system that sorts your unpaid client invoices by how far past due they are. Instead of wondering why the bank balance is dangerously low, a quick glance at this report highlights exactly which clients are stalling so you can speed up collections before a cash crunch hits.

Mastering these collection timelines transforms chaotic guessing into proactive financial planning. You can confidently predict if you will have enough cash to buy inventory next month without taking on emergency debt. Moving from daily cash survival to long-term strategy naturally leads to your next milestone: The Power of the Three-Statement Health Check: P&L, Balance Sheet, and Cash Flow.

The Power of the Three-Statement Health Check: P&L, Balance Sheet, and Cash Flow

Tracking daily deposits is a great start, but true business intelligence requires zooming out. When relying solely on a bank balance, you cannot identify if your business is actually growing or just staying busy. To spot trends in overhead expenses before they eat your profit, and to comfortably meet the financial reporting requirements for LLCs, you need structured statements. Professional accounting services build and interpret these documents so you can make confident, data-driven decisions.

Think of these structured reports as a comprehensive medical chart for your company, divided into three main areas:

- Profit & Loss (The Scorecard): This tracks your revenue minus your expenses over a specific period to reveal your true operating margins.

- Balance Sheet (The Health Check): This provides a snapshot of what you own (assets) and owe (liabilities) today. The difference between those two numbers is your “Equity”—what the business is actually worth to you personally.

- Cash Flow Statement (The Oxygen Meter): As discussed, this tracks the literal movement of dollars to ensure you can pay bills on time.

Tracking your equity and profit margins turns financial anxiety into strategic power. Armed with an accurate picture of your business’s health, you are perfectly positioned to lower your upcoming IRS bill legally. This proactive stance naturally bridges into your next critical step: Tax Planning vs. Tax Preparation: Saving Money Before the Year Ends.

Tax Planning vs. Tax Preparation: Saving Money Before the Year Ends

Most business owners view April as a stressful finish line, but treating taxes as a once-a-year event leaves money on the table. Tax preparation simply records history to tell the IRS what happened. Conversely, using proactive tax planning strategies for entrepreneurs acts like a financial GPS, guiding strategic moves before December 31st to actively shrink your future bill.

Knowing how the IRS treats your money is the foundation of this proactive approach. When maximizing small business tax deductions, you must clearly distinguish between deductions and credits. A deduction subtracts from your income bucket so you are taxed on a smaller amount. A credit acts like a gift card applied directly to your final bill, offering a dollar-for-dollar reduction that instantly protects your hard-earned profit.

Selecting the optimal business structure unlocks even deeper savings once your revenue grows. For example, a successful freelance designer might make an “S-Corp Election”—a specific tax status changing how the IRS categorizes their income. Instead of paying hefty self-employment taxes on every single dollar, this election lets them take a reasonable salary and pull the rest as tax-advantaged distributions.

Upgrading your legal structure does require a shift in daily operations. Because an S-Corp status mandates paying yourself a formal W-2 salary, your responsibilities expand from simple owner draws to official employee compensation. This exciting growth milestone naturally leads to mastering these new obligations in Beyond the Paycheck: Managing Payroll Processing and Tax Filings.

Beyond the Paycheck: Managing Payroll Processing and Tax Filings

Transitioning from a solo founder drawing a simple salary to an official employer adds exciting capacity, but it also triggers strict rules for payroll processing and tax filings. When you run a formal payroll, you do not just write a check. You act as a temporary bank for the government by holding back portions of your workers’ pay—known as “Trust Fund Taxes”—to send to the IRS. Automating this system is the safest way to guarantee IRS tax compliance for startups, because missing your quarterly Form 941 (your employer tax return) triggers expensive “failure to deposit” penalties.

To keep your growing operations completely legal, you must clearly track these critical payroll components:

- Gross pay: The total amount a worker earns before any deductions.

- Tax withholdings (federal/state): The income taxes you collect and submit on the worker’s behalf.

- Unemployment insurance: Along with worker’s compensation, these are state-level safety nets you must fund for standard employees.

- 1099 vs W-2 status: A W-2 employee follows your set schedule, while a 1099 contractor operates their own independent business. Misclassifying workers to avoid taxes brings severe fines.

Mastering how you compensate your team protects your hard work from internal audits and keeps your focus on growth. However, payroll is not the only area where crossing state lines complicates your business responsibilities, which we must navigate next in Digital Borders: Navigating Sales Tax Nexus for Online Sellers.

Digital Borders: Navigating Sales Tax Nexus for Online Sellers

Selling products online feels like operating without borders, but state tax departments disagree. Since the landmark Supreme Court Wayfair decision, states can charge sales tax even if you have no physical building there. This concept is called “Nexus”—a legal connection meaning you are virtually standing in another state, and that state expects a cut of your sales.

Three specific activities typically trigger this connection: holding physical inventory in a state, hiring an employee there, or crossing a local sales threshold. This last trigger is called Economic Nexus, which usually activates after $100,000 in revenue or 200 separate transactions within that state. For example, a home-based candle maker in Ohio might suddenly owe sales tax in Texas just because a viral video drove a massive surge of Texan orders. Monitoring these invisible borders is a major reason growing businesses hire professional accounting services for small businesses in the United States.

Luckily, you do not have to calculate these varying rates manually. Modern financial software automatically tracks buyer locations, applies the correct tax, and handles “remittance”—the process of sending those collected funds to the proper state agency. Automating this protects your overall IRS tax compliance for startups without demanding late-night math sessions. With your required tax payments running smoothly in the background, you can turn your focus toward keeping more of your revenue in Maximizing Every Dollar: A Guide to Small Business Tax Deductions.

Maximizing Every Dollar: A Guide to Small Business Tax Deductions

Building a profitable business means keeping what you earn. The secret to maximizing small business tax deductions lies in mastering two IRS concepts: “ordinary” (common in your industry) and “necessary” (helpful for growth). For large, necessary items like a new commercial laptop, you will also encounter depreciation—a tax rule that spreads the expense deduction over the equipment’s useful lifespan instead of claiming the massive cost all at once.

Once you know these rules, finding hidden savings becomes easy. Here are five top deductions owners often miss:

- Home Office (square footage)

- Business Mileage

- Professional Development

- Software Subscriptions

- Marketing

If you work from a spare room, the IRS “Simplified Method” makes claiming your office space effortless. Instead of calculating a complex percentage of your monthly utility bills, you simply multiply your workspace’s exact square footage by a standard flat rate.

Protecting these valuable write-offs requires ditching the disorganized shoebox of paper. Setting up a basic system for digital receipt capture on your phone secures your proof instantly, ensuring you can confidently survive an IRS audit. While smart tax planning strategies for entrepreneurs begin with these daily habits, your financial needs will eventually grow. When that happens, you will reach a critical turning point: QuickBooks vs. A Pro: When Software Isn’t Enough.

QuickBooks vs. A Pro: When Software Isn’t Enough

Connecting your business checking account to software feels like magic, thanks to bank feeds that automatically import your daily transactions. However, a program is just a tool, not a financial strategist. If the system guesses incorrectly and labels an expensive client dinner as a personal meal, it creates a reconciliation error—a frustrating mismatch between your actual bank balance and your digital records.

Spotting the warning signs of a DIY data disaster can save you thousands. You should seriously evaluate QuickBooks vs professional accounting services if you notice three distinct red flags: you see negative balances in expense categories, you actively avoid looking at your financial reports because the numbers seem suspicious, or you lose precious weekend hours untangling categorization mistakes instead of resting.

Upgrading to a “tech stack” approach—powerful software paired with a human expert—turns stressful data entry into valuable business intelligence. When a pro conducts a monthly review, they fix those hidden errors and help you understand exactly which services are actually profitable. Eventually, you will need to weigh virtual accounting services vs local firms for this critical oversight, bringing you to Choosing the Right Partner: CPAs vs. Virtual Firms vs. Local Bookkeepers.

Choosing the Right Partner: CPAs vs. Virtual Firms vs. Local Bookkeepers

Finding your financial partner starts with defining your “Minimum Viable Service”—the exact help you need right now without overpaying. Weighing virtual accounting services vs local firms means balancing your need for face-to-face reassurance against cloud-based speed. As you step away from DIY software, consider your three primary options:

- Local CPA: Offers high trust and strategic tax advice, but comes with higher costs and traditional office hours.

- Virtual Firm: Provides scalable, tech-forward solutions, though you trade physical handshakes for video calls.

- Freelance Bookkeeper: Delivers low-cost daily data entry, but has a limited scope and cannot legally file taxes.

Once you select a path, choosing a CPA for small business success requires testing for a true partnership fit. You can evaluate them by asking three critical questions: “How often will we communicate throughout the year?”, “What software ecosystem do you require?”, and “Can you explain a complex tax deduction simply?” Their answers will instantly reveal if they view you as a valued collaborator or just another folder on their desk.

Making the right hire ultimately frees you to focus on your customers rather than stressing over compliance. Naturally, budgeting for this essential support is your next priority as a growing entrepreneur. That brings us directly to How Much Does Peace of Mind Cost? The Truth About Accounting Fees.

How Much Does Peace of Mind Cost? The Truth About Accounting Fees

Every hour spent wrestling with spreadsheets is an hour you aren’t selling to a new customer. When entrepreneurs ask how much do small business accountants cost, they often forget to calculate their own opportunity cost. If your time is worth fifty dollars an hour and you spend ten hours a month on bookkeeping, that “free” DIY approach actually costs you five hundred dollars in missed sales.

Modern financial professionals have largely moved away from unpredictable hourly billing that punishes you for asking quick questions. Today, the most reliable accounting services for small businesses in the United States use value-based pricing. This model relies on a fixed retainer—a flat, predictable monthly fee tied to the specific outcomes and peace of mind you receive, rather than the raw hours an accountant sits at their desk.

Budgeting for this help usually means choosing between a hefty tax season premium for a once-a-year rush job or investing in smoother year-round support. Once your foundational tax needs are running on autopilot through a predictable monthly schedule, you might realize your growing company requires deeper financial forecasting. That is exactly when it makes sense to explore the fractional CFO: scaling your business without the six-figure salary.

The Fractional CFO: Scaling Your Business Without the Six-Figure Salary

Hitting a major revenue milestone is thrilling, but it usually brings a new kind of headache. Your regular accountant accurately tracks what already happened on your financial statements, but now you need someone to predict the future. Enter the fractional CFO—an experienced financial executive you hire part-time. Instead of paying a massive salary for a full-time Chief Financial Officer, you pay a fraction of the cost for high-level strategy. This executive guidance often pays for itself by uncovering operational efficiencies that can reliably increase your profit margin by 5 to 10 percent.

This transition moves your operations from simple survival to active financial planning. Fractional CFO services for growing businesses focus strictly on forward-looking growth levers, including:

- Budget vs. Actuals analysis: Comparing your planned spending against your real-world numbers to catch cash leaks early.

- Pricing strategy: Using data-driven decision making to clearly identify which products to scale and which unprofitable services to kill.

- Capital raising prep: Structuring your financials so they are completely investor-ready.

- Exit planning: Building long-term business value for an eventual sale.

With these strategic systems running, your company becomes a highly proactive machine. However, even the most brilliant forecasting still relies on perfectly finalized historical data. Before mapping out next year’s lucrative strategy, you must close out your current calendar year correctly. This brings us directly to the year-end tax preparation checklist: starting your new year with a clean slate.

The Year-End Tax Preparation Checklist: Starting Your New Year with a Clean Slate

December brings holiday cheer, but for small business owners, it often triggers the dreaded “January Scramble.” Instead of panicking over faded paper, executing a tactical year-end tax preparation checklist clears the decks for the new year. This proactive approach prevents costly filing errors and keeps your focus entirely on future growth rather than past mistakes.

Hitting a roadblock here usually prompts founders to ask, “do I need an accountant for my small business?” Whether you hire professional help or tackle it yourself, you must complete this five-step closing process:

- Receipt organization: Try the “Receipt Audit” trick—randomly select three ledger expenses and ensure you can find their matching documentation in under a minute.

- 1099-NEC preparation: Gather a Form W-9 (a basic tax ID request) from contractors before paying them, making it easy to report non-employee compensation over $600 to the IRS.

- Final bank recs: Verify your accounting software matches your real-world bank statements to the penny.

- Inventory count: Record exactly what physical products remain unsold on December 31st.

- Mileage logs: Tally all business-related driving to secure your travel deductions.

Completing these administrative tasks does more than just keep the IRS happy; it provides a crystal-clear picture of your true annual profit. By closing out the year cleanly, you set the stage perfectly for your ultimate business transition: moving from spreadsheet stress to financial mastery.

Conclusion: From Spreadsheet Stress to Financial Mastery

You started this journey looking to untangle the dreaded “shoebox of receipts,” but you now recognize the profound shift from merely filing taxes (compliance) to actively steering your company’s future (growth). Using professional accounting services for small businesses in the United States does much more than keep you out of trouble with the IRS; it acts as the financial GPS for your business. When you view these services as a strategic investment rather than a painful cost, you unlock insights that drive true profitability.

With the mechanics of this financial engine clear, it is time to take control. You do not have to overhaul your entire operation overnight to start seeing immediate results. Instead, transform this new knowledge into momentum by following a simple 30-day roadmap designed to build your confidence and clarify your numbers.

Start with these progressive steps to gain immediate control of your business data:

- Week 1: Organize your accounts by strictly separating personal and business finances into distinct bank accounts.

- Week 2: Research basic bookkeeping software or begin vetting local professionals to match your growth stage.

- Week 3: Take the next step by choosing a CPA for small business strategy and scheduling an introductory consultation.

- Week 4: Establish a monthly routine to review your cash flow, upcoming expenses, and recent profits.

That final step—committing to a monthly “Financial Date” with your business data—is where the real magic happens. By setting aside just one hour each month to sit down with a coffee and review your numbers, you strip away the anxiety previously associated with bookkeeping. Each time you check in on your profit margins, you build the financial muscle needed to make smarter, faster decisions for your craft.

Running a business takes immense courage, and you no longer have to navigate the financial side in the dark. With a clear view of your financial health and the right professional partners in your corner, that end-of-year tax panic transforms into profound peace of mind. You now have the foundational knowledge to stop guessing, start planning, and step confidently into your business’s most profitable chapter.